Five Below: A regional to national expansion story

Brief Overview

Five Below represents a compelling opportunity in the discounted retail space with a sustainable square-footage growth story, highly productive go to market model and limited competition from the e-commerce threat. Operating 1,191 stores in 40 states, Five Below is in the early stages of a national rollout that will couple increased density in new markets along with new geographies. Management is laser focused on its treasure hunt experience and growing the store base quickly, but tactically improving brand recognition to support further growth.

Business Model

Value Proposition

A unique store experience: to understand the Five Below concept you have to go back to the start. In the early 2000s, the two founders (David Schlessinger and Tom Vellios) recognized that there was a market opportunity to serve the needs and wants of pre-teens. They landed on the idea of creating a unique place where kids aged 8-14 could go and spend their allowance money on stuff they wanted, a place where kids could graduate from the toy store to a store where they could afford everything.

Five Below’s purpose is to serve as a practice ground for up-and-coming consumers, pre-teens who have the fortitude of having an allowance and who are trying to figure out the most satisfying ways of spending it. Five Below does not necessarily offer unique items for sale, nor does it offer a lower price than other competitors. What the store has managed to accomplish is to edit the endless offerings targeted at teens and preteens and assemble in one place everything trendy that can be sold for five dollars or less.

With the wide assortment of non-essential items, Five Below has revolutionized the retail industry and has created a new category of retailer, one that strives to have fun in a consumer world often driven by necessity. The shopping experience relies on surprise as much as affordability. “If you spend time in a dollar store or mass merchant like Target or Walmart, it’s not really about letting go because you’re there to meet your needs.” said David Makuen, ex executive vice president of marketing and strategy. A good analogy to understand the behavior of people that shop at a Five Below store is that of an amateur gambler. Both are paying a price to be entertained. Five Below knows this, and it is one of the reasons the company has been so successful. They figured out that instead of addressing a consumer need, they just have to position themselves to capture a consumer behavior.

Compared to other retailers, a Five Below store showcases bright colors, playful slogans, and pumping music. The company also encourages its customers to play with the basketballs, participate in slime-making contents and test drive ratio-controlled cars.

Teen and pre-teen focused: Five Below’s customer base is large, but the company primarily targets the generation Z. This age group, which is known as Gen Z, is the third largest cohort in the U.S., and is the most racially, ethnically, and sexually diverse generation in history. Gen Z is expected to make up 20.2% of the U.S. population by 2022, or 68.2. million. There is a reason why the company specifically targets this customer segment. Unlike Millennials that that are cash strapped due to the increased cost of housing and ever rising student debt, the majority of Gen Zers are still living at home, and as a result their income isn’t drained by other expenses.

In addition, Gen Z tends to buy via social media and influencers, something that plays to Five Below’s core competency of selling trendy products that are often made popular via Instagram/Snapchat/TikTok. Gen Zers spend about three hours a day on social media, and 40% of them say that social platforms have heavily influenced what they purchase, as opposed to other generations that are more influenced by family, friends, online reviews and tv ads.

This age group also performs product research on social media differently. Millennials approach the task by consulting their social connections to get a sense of product functionality, while Gen Z looks out for specific individuals that they believe know about the product. This explains why more than 50% of Gen Zers are likely to buy a product or service if an influencer recommends it. "Gen Z places a lot of trust in individual voices for news and information to help them form their opinions," says Monica Deretich, retail industry advisor to CM Group.

Lastly, Gen Zers prefer brands that are able to merge the digital and in-store experience. About 75% of Gen Zers shop on their smartphones, but they still prefer to shop in a physical store. This age group sees shopping as a social expedition, and they prefer brands that can offer a unique and immersive experience.

Trend Merchandise with Broad Appeal: Five Below takes a unique approach to its in-store offerings that differentiate the retailer from its competition. The chain organizes its store around 8 categories or worlds: Tech, Create, Play, Candy, Room, Style, Party and New & Now. These eight categories give the value retailer enormous flexibility to capture new trends as they emerge. In addition, by offering items for a relatively short amount of time, the retailer is seeking to take advantage of the customer’s perception of hype and exclusivity. This approach makes Five Below unique among its peers, who usually try to provide value to their customers in terms of discounts as opposed to products that cannot be found anywhere.

A lot of items on the store can be characterized as being a mix of splashy and functionality. It is an astute approach on the part of the retailer given that it helps to alleviate the guilt and makes the purchase that much easier.

Investment Thesis

1) Reinvestment Moat

When the specialty value retailer first came to market in July of 2012, the company telegraphed its ambition to open more than 2,000 stores over time from the 192 locations that were open mostly in the eastern half of the United States. Fast forward to today, and the company has managed to achieve an impressive 20% CAGR in unit growth over the period.

During fiscal 2021, Five Below added 171 net new stores to bring the current footprint to 1,191 stores. There is still ample opportunity for white space in the western part of the country, such as in California, which currently accounts for only 7% of the store base. The company has been investing heavily in infrastructure to support its planned growth by expanding the number of distribution centers from 2 in 2018 to 5 in 2021. The current set up has the capacity to support 2,000 stores.

Equity returns for retailers are usually correlated to comparable stores sales, but in the case of Five Below, investors would be better off by ignoring this tendency. This is because 80% of the sales growth during the past decade has been driven by sales from new stores, which in my opinion is a more predictable source of growth given consistent store productivity metrics. By this I mean consistency of sales per store by vintage and by geography. New stores usually ramp up sales quickly to a level that is usually around 90% of the average store revenue level.

At the most recent investor day presentation, the company laid out its Triple Double Vision (growth algorithm), that calls for a triple of the store base to 3,500+ by 2030, while doubling sales and bottom line by 2025. The target seems achievable as there are roughly 15,840 Dollar Tree stores in the US, which also focus on merchandising discretionary products to higher income households.

2) Merchandising sourcing serves as a barrier to entry:

a) Five Below merchandising strategy is based on the idea of scaled economies shared (SES), a concept popularized by the famous investor Nick Sleep of Nomad Investment Partnership. The strategy entails improving its offering to customers in order to win wallet share over the long-term, rather than pricing its products to maximize per unit-profit in the short-term. Five below is embracing delayed gratification (via long-term shareholder value creation), while giving customers instant gratification (via increased value proposition of the goods provided).

So how exactly is Five Below able to improve the quality of its offering while at the same time maintaining the $5 price point? It all starts with concentration of product offering, which leads to better procurement terms. The chain’s stores typically contain around 4,000 SKUs, significantly less than some of its rivals (Dollar Tree at 7,000). This strategy allows the retailer to order in a size not otherwise possible for a chain with just 1,191 stores. As a result, the chain becomes a valuable partner for its suppliers, while driving scale efficiencies in shipping and logistics costs. This leads to a flywheel effect, further adding to the chain’s value-oriented strategy.

b) Ability of the merchandising team to quickly identify and capitalize on trend right merchandise based on years of experience focusing on the pre-teen and teen category: Even though product trends are transitory, Five Below has demonstrated an ability to quickly respond to customer demand, leaving its product assortment current even as the items themselves are constantly in flux. Given the challenges in predicting trends, the retailer has focused its attention on swiftly responding to them, benefiting from a flexible sourcing strategy and an economically advantaged distribution system. As an example, the retailer altered its product assortment during the pandemic to take advantage of the increased demand for cleaning solutions and home-related items, attracting parents and young adults that were looking to combine shopping trips. Lastly, the retailer’s opportunistic sourcing and distribution strategy allows it to exploit other retailer’s excess ordering.

3) Five Beyond and other initiatives will lead to increased customer spend

The Five Beyond idea was born out of the discounter’s test run of a higher-priced section within the store called Ten Below. In 2019, as the retailer was facing higher costs in key product categories such as technology, the chain started experimenting with selling products above their $5 price range.

The concept gives Five Below much needed flexibility to meet customer demand for products, like electronics, which might have fallen outside the price promise as well as drive improvements in margins where the chain sees opportunities.

Five Beyond stores are currently in 30% of locations and the chain has the aspirations to incorporate the store within a store concept in 80% of locations by 2025. Customers that shop at Five Beyond are usually older than the core demographic, and their basket size is 2x that of Five Below only shoppers.

Other notable initiatives that I believe will help the retailer capture wallet share and reignite same store sales growth are a) their goal of being the destination for milestones for teens and pre-teens b) capture incremental dollar sales from customers as they age into their early twenties. The retailer is focused on strategic moments in a young person’s life identified by products such as balloons for commemorating events, room assortments to adorn personal spaces, accessories for personalizing a first car, pet items, and ear piercing.

The introduction of Five Beyond serves as an example of how the firm pivoted to play offense, instead of being pressured by the difficult macroeconomic environment.

4) Relatively less rivalry intensity than for other retail categories

Comparable to other dollar stores, Five Below’s low price points help insulate it from digital rivals, especially as online sellers need to absorb shipping costs. In addition, impulse-oriented visits and merchandise discovery account for the vast majority of purchases and is something that is extremely difficult to replicate online. The fast-changing nature of the merchandise incentives consumers to return and helps keep the interest of the preteen and teenager customers that the firm targets. The search for value and low-price points promotes store traffic while improving the retailer’s ability to exploit on routine shipping trips.

Economics/Financials

Growth and Profitability

Five Below is a company that is already profitable, but it has further room to improve its margins. The graph below illustrates Five Below’s earnings power before and after taxes. Both before and after-tax measures of profitability have improved since the company went public in 2012.

Five Below has managed to generate operating leverage over time as the graph above illustrates. As the company has scaled its operations, profit margins have expanded, indicating efficiency in converting sales to profit. Profit margins have risen by 623 basis points to 9.79% in 2021. Total revenues have grown by 14x during this period, from $197.19 million to $2.85 billion. Most importantly, the bottom line for Five Below’s has grown by a factor of 39x, from $7.02 million to $278.8 million. No wonder the stock has compounded at 16% per year, outpacing the S&P 500 by 265 bps annually.

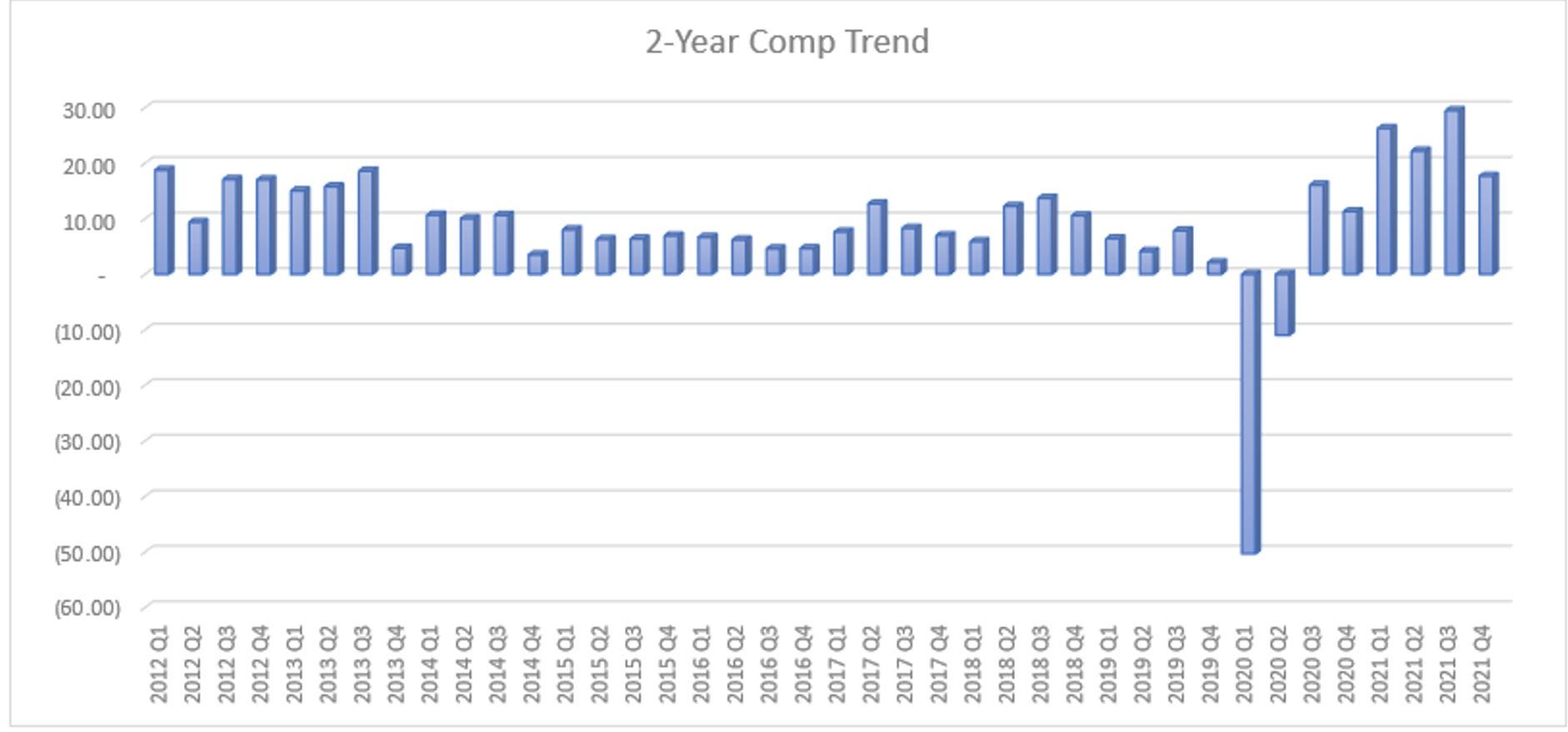

Growing sales by opening new stores is great but generating a higher level of sales from existing stores is also important for a retailer as it signals ongoing relevance to consumers and strength in competitive position. Five Below same store sales (SSS) on a 2-year stack basis have grown strongly over the past 10 years. If we segment the data by 5-year periods, we can see that there has been no deceleration in the SSS growth. From 2012 Q1 through 2016 Q4, Five Below’s median SSS growth was 8.68%. For the most recent 5-year period, that figure stood at 9.42%. Some investors have grown more skeptical of the concept recently given the deceleration in the year over year SSS growth. However, the data below makes it clear that is not case, and that the long-term opportunity remains bright for this company.

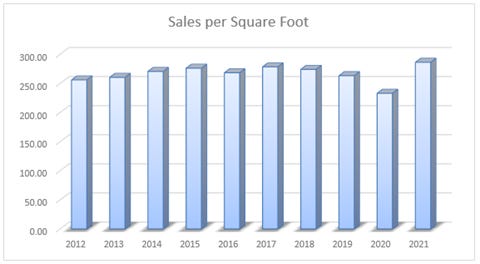

Performance measures on a per store basis show a positive trend. Sales per store have increased by 34% from $1.9 million in 2012 to $2.6 million in 2021. Similarly, sales per square foot show a steady progression, increasing from $256 to $286. EBITDA per store has almost tripled, growing from $217,000 to $603,000, and finally, Net Income per store has risen from $92,000 to $252,000.

An important profitability indicator that can provide valuable insights into the company’s operations is return on equity (ROE). In general, a higher ROE is preferred, as high ROE companies can produce more earnings and cash flow than can be used to fund a higher level of growth, keep the company on a strong financial footing, and provide excess cash that can be used to reward shareowners through dividends and share buybacks. In addition, it can be argued that the intrinsic value of high ROE companies grows at a faster pace than low ROE companies.

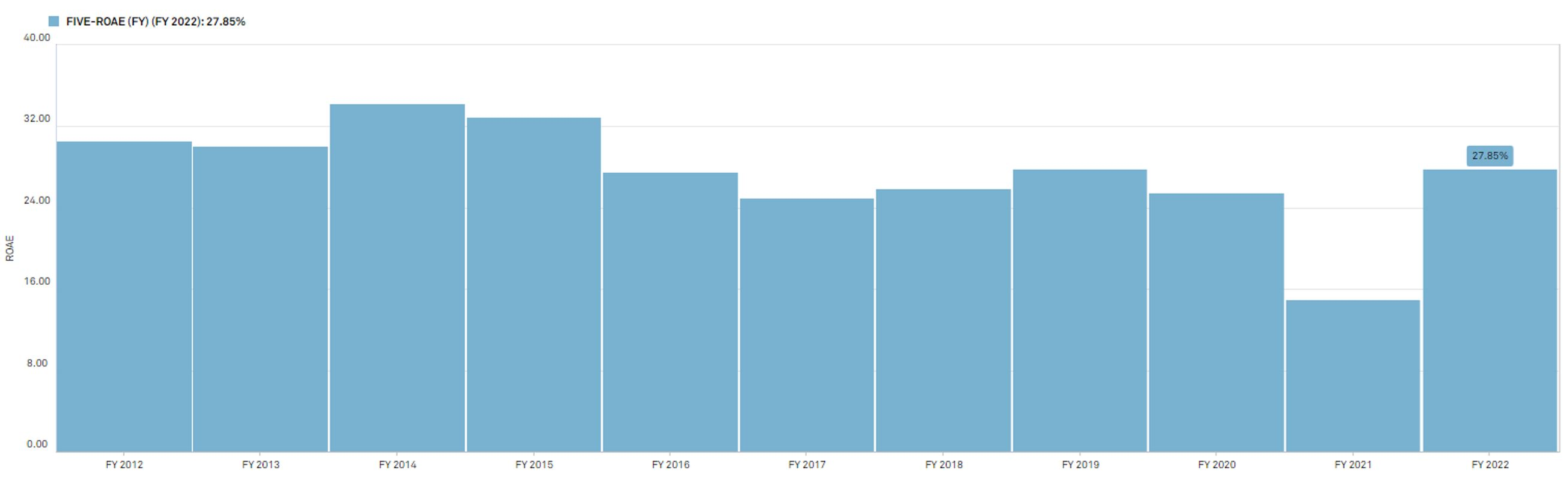

The chart below illustrates that Five Below has consistently generated an impressive ROE above 25% (albeit during the pandemic) through different economic environments.

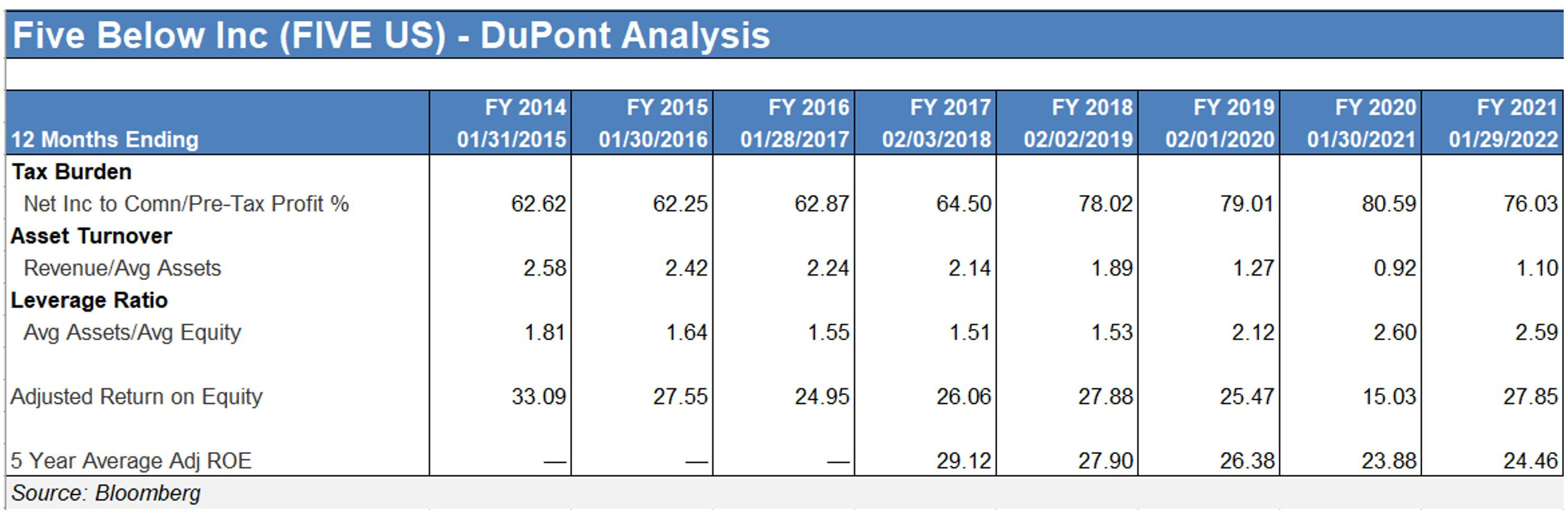

To understand what is driving such exceptional returns on equity we can use the DuPont Analysis to break down ROE into several parts. We can see that the trend in the tax burden is positive, given that a greater share of EBT dollars are flowing through to the bottom line. The tax burden has risen from roughly 63% in 2014 to 76% in 2022. On the other hand, asset turnover has deteriorated sharply since 2014, falling from 2.58 to 1.10. Lastly, the amount of leverage that the retailer is employing has increased somewhat, perhaps as management has more confidence in the long-term outlook for the company and the relevance of the concept.

A final note on return on equity is warranted. As some of the research has demonstrated, a high ROE is desirable because if the company is truly generating profits in excess of the cost of equity capital, then it is creating value for shareowners. Assuming a conservative cost of equity of 15% for the company and the 5-year average ROE of 24.46 for the most recent year, Five Below is generating an excess return of 9%. However, it is not enough to generate a high return, consistency of the return is also of paramount importance and is something that Five Below has managed to achieve.

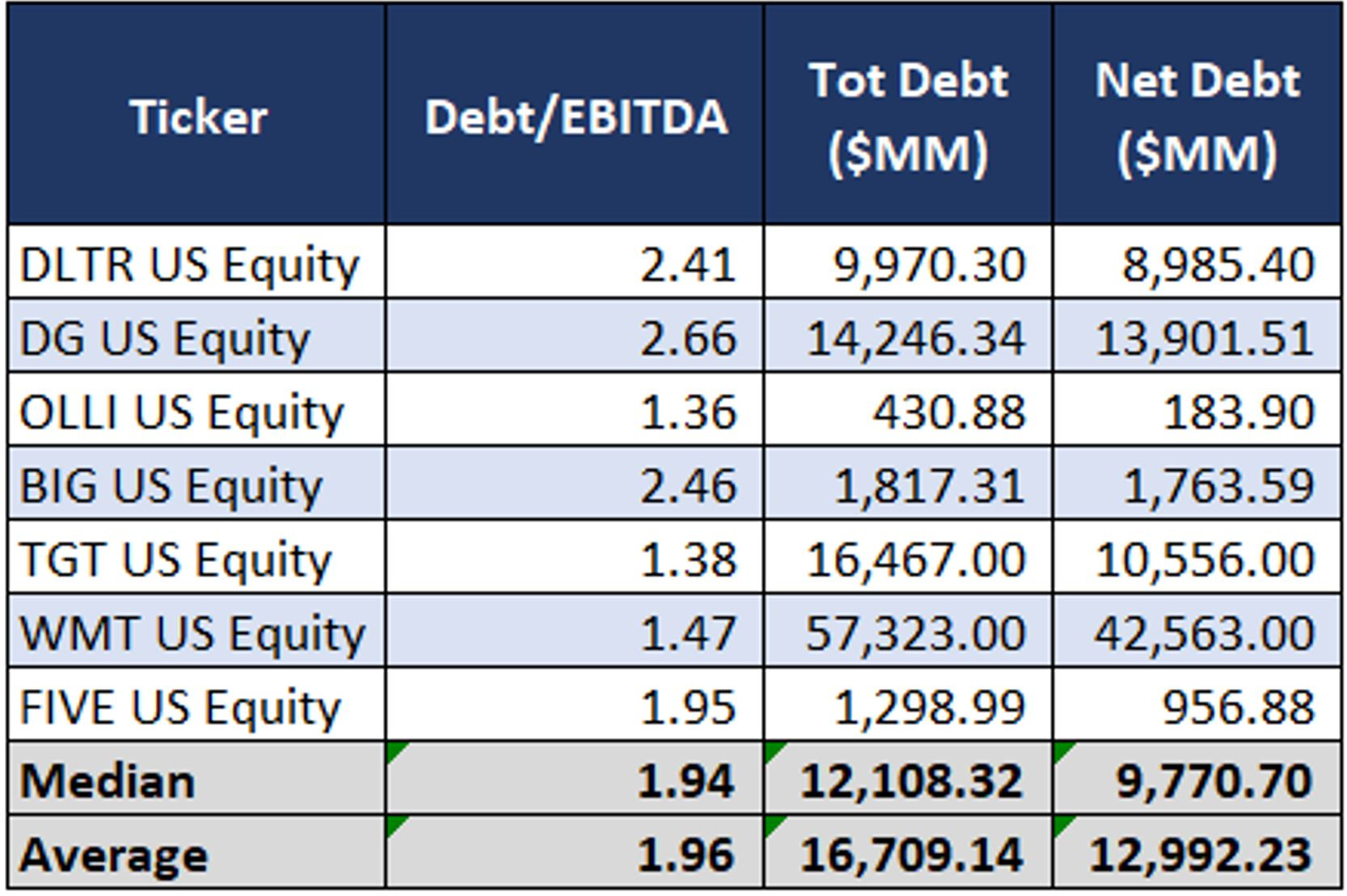

To conclude this section, it is worth looking into the company’s capital structure and how it is financing its operations and expansion opportunities. On a Debt relative to EBITDA basis, Five Below is employing a similar amount of leverage as the peer group.

Valuation

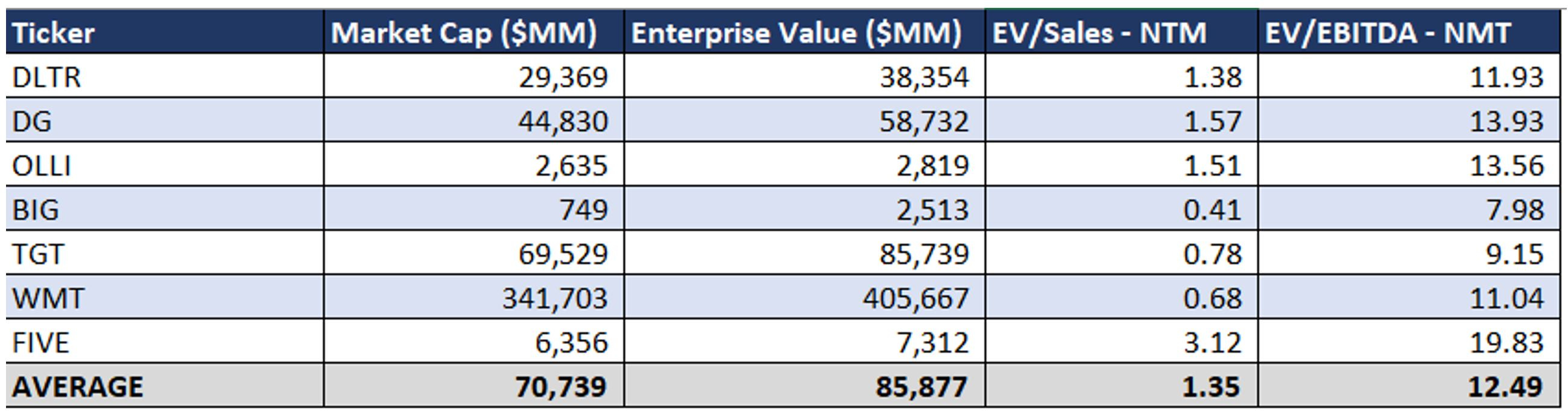

Against its peer group of discounted retailers, it appears as if Five Below is relatively overvalued. On an Enterprise Value basis, the retailer is trading at 3 times forward Sales, while the average for the peer group stands at 1.35. However, multiples in and of itself mean nothing without context for relative growth rates going forward and differences in margin structures.

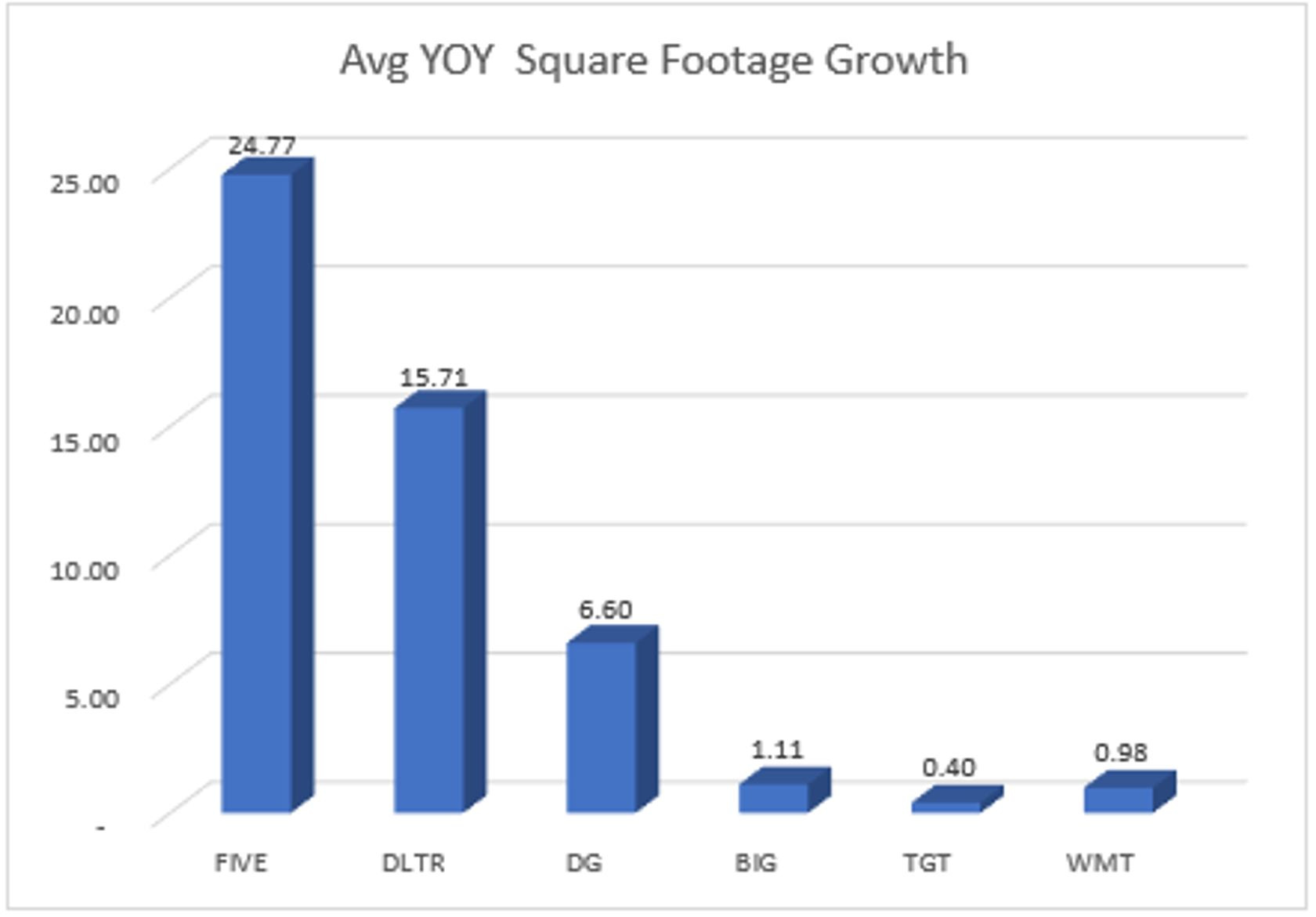

As far as growth goes, Five Below has shown strong growth and very strong profitability (as evidenced in the company’s sales and earnings growth, as well as return on equity). What’s more, Five Below has grown its retail footprint by a CAGR of 25% over the past 12 years, as measured by the average year over year growth rate in square footage. That compares exceptionally well against best-in-class operators such as Dollar General, Walmart, and Target in the discount retail space.

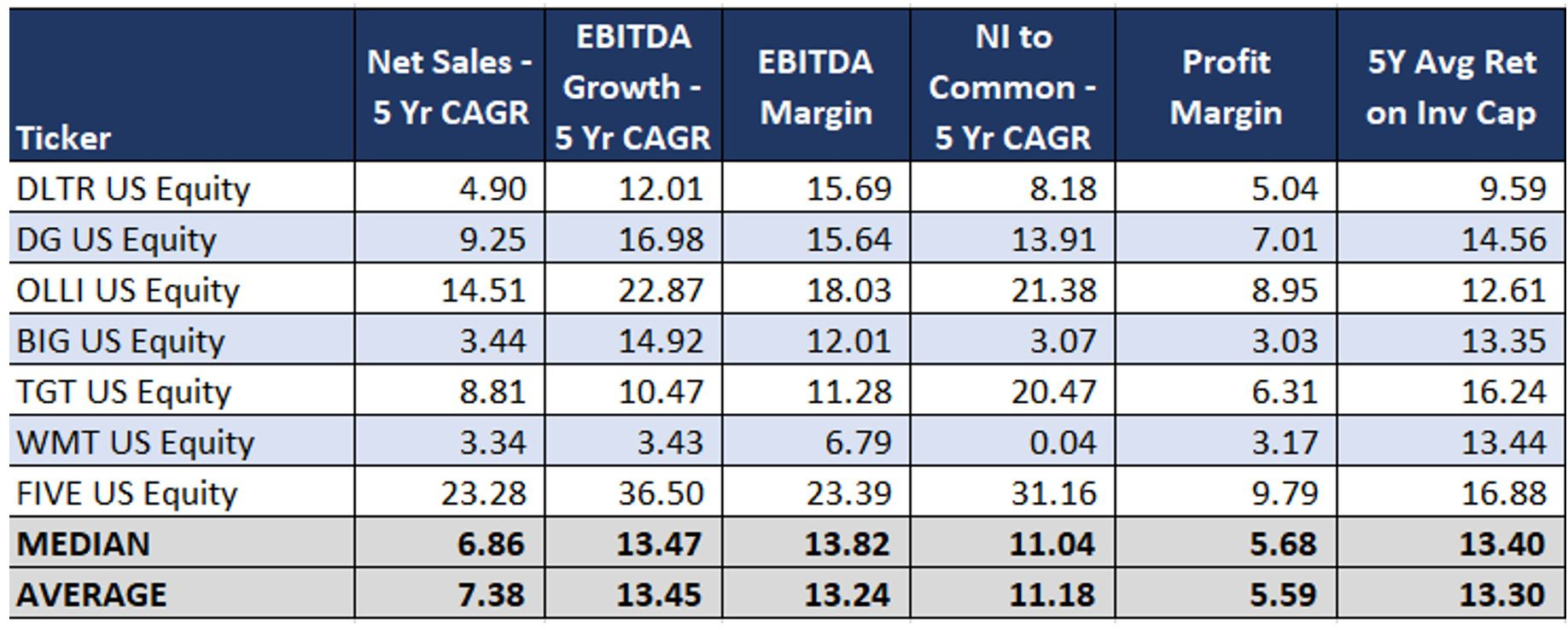

The table below compares some growth metrics as well as profitability for Five Below against its peers. If we look at the growth in fundamentals, Five Below has outperformed its competition by growing Sales at more than 3 times the rate of the peer group median, and EBITDA and bottom line at more than twice the rate. On a margin perspective, Five Below has shown the ability to execute well against its long-term growth algorithm without compromising profitability. EBITDA and Profit margins are superior to those of its peers. Lastly and important for value creation, its 5-year average return on capital stands at 17%, comfortably exceeding rivals.

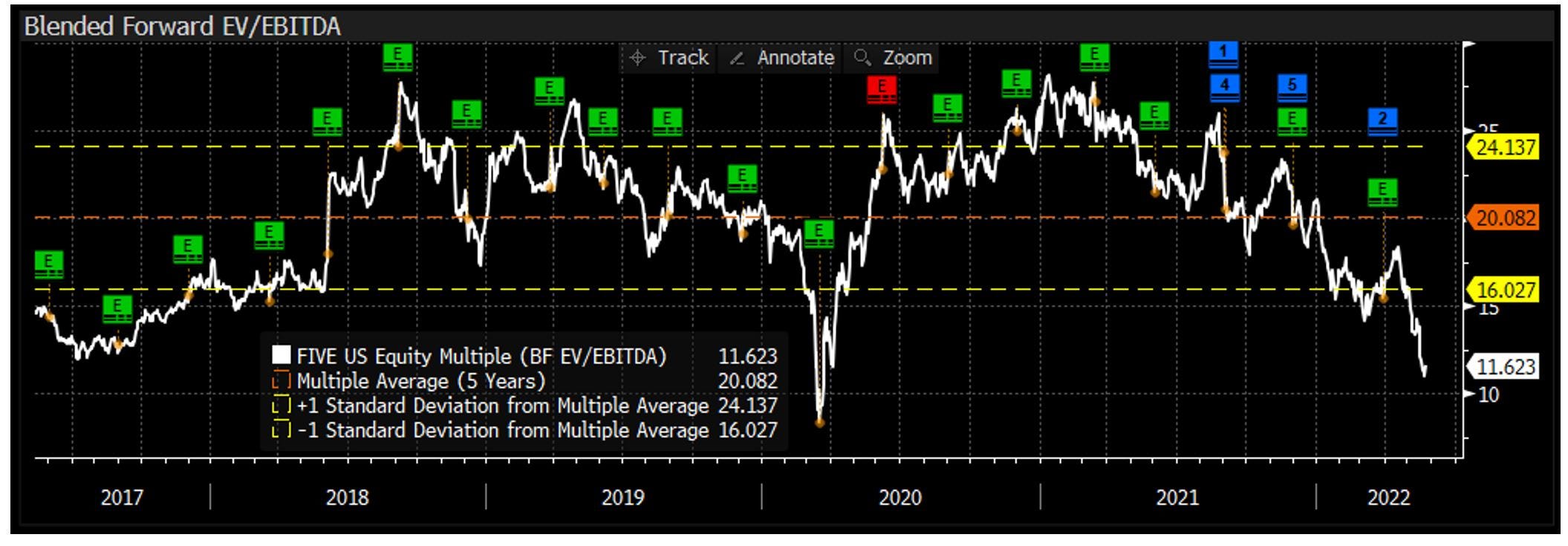

We can also get a sense for relative value by observing how the market has priced the retailer through different economic environments. As the chart below illustrates, Five Below is currently trading cheap relative to its history. The current EV to forward EBITDA multiple of 11.6 is at a 42% discount to its 5-year average and more than 2 standard deviations below the mean. Other multiples, such as EV to forward Revenue, and EV to EBIT are in a similar ballpark. Today’s multiple is not that far off from the lows reached during the covid induced crash, when the chain was forced to close all its retail locations to comply with government-imposed mandates. The market is pricing in a lot of pessimism at the moment given concerns about deteriorating economic conditions affecting discretionary spending, and the uncertain outlook for inflation.

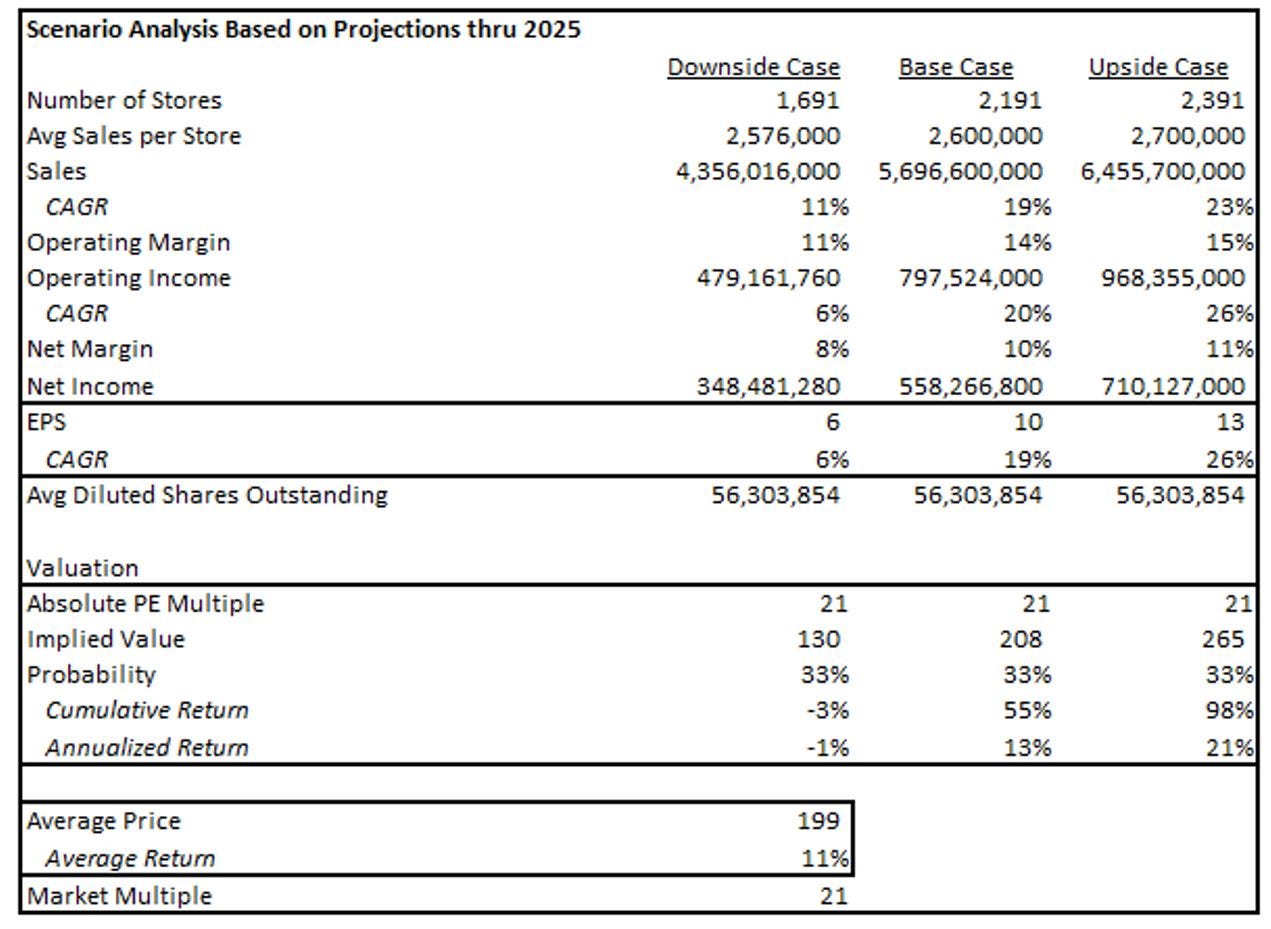

Based on the above, what kind of returns is Five Below likely to generate going forward? Below is a scenario analysis as of June 7th to help answer this question. My base case has the retailer generating annualized returns of 13% through the end of 2025 based on the following assumptions:

The retailer’s Triple Double Vision comes to fruition and its retail footprint expands by 1,000 new stores.

Average sales per store expand modestly from the current $2.58 million to $2.6 million as the retailer’s brand awareness continue to improve driven by its clustering strategy and advertising efforts.

Operating margins expand to 14% driven by scales benefits, efficiencies in its distribution networks and fixed cost leverage.

Net margins expand by 21 bps to 10%.

Its multiple of earnings declines from the current 27x to a market multiple of 21x.

Under this scenario, Five Below would compound capital at 13% annually, driven by exceptional earnings growth.

Based on the below, the probability adjusted annualized return for Five Below is 11%, matching historical US equity market returns.

For long-term investors willing to look out 3-5 years, the current set-up offers an attractive entry point for a high-quality company with ample runway for growth.

Conclusion

I believe that Five Below is a high-quality company. It earns outstanding returns on capital that are underpinned by economies of scale, has ample room for growth and its management has done an outstanding job of capital allocation. As just mentioned, the outlook for the retailer is to potentially double the current store count. The company’s customer base is expanding, capital is being disciplined allocated, returns are very strong, and its unique business model and merchandising strategy protects it from e-commerce rivals. New locations will more than likely help continue the upward trend in top and bottom-line growth. Finally, I believe that the shares are priced at a reasonable valuation given its growth prospects and competitive position.

This was great, gonna share this with my own readers in my next curation letter.

Hello there,

Huge Respect for your work!

New here. No huge reader base Yet.

But the work has waited long to be spoken.

Its truths have roots older than this platform.

My Sub-stack Purpose

To seed, build, and nurture timeless, intangible human capitals — such as resilience, trust, truth, evolution, fulfilment, quality, peace, patience, discipline, relationships and conviction — in order to elevate human judgment, deepen relationships, and restore sacred trusteeship and stewardship of long-term firm value across generations.

A refreshing take on our business world and capitalism.

A reflection on why today’s capital architectures—PE, VC, Hedge funds, SPAC, Alt funds, Rollups—mostly fail to build and nuture what time can trust.

“Built to Be Left.”

A quiet anatomy of extraction, abandonment, and the collapse of stewardship.

"Principal-Agent Risk is not a flaw in the system.

It is the system’s operating principle”

Experience first. Return if it speaks to you.

- The Silent Treasury

https://tinyurl.com/48m97w5e